Audio By Carbonatix

Miami is, mythically, a place where immigrants from around the world come to work, save money, and build wealth.

In reality, though, it appears the local and national economies are so unbelievably broken that people are mostly coming here to work themselves into the ground. According to new data from the investment-advising firm Unison, the typical Miami resident needs to save money for a staggering 36 years in order to afford a down payment on a home, provided the household is saving 5 percent of its annual income. In comparison, the national average is only 14 years. Miami is tied with New York City for fourth on the list – they come in behind Los Angeles (43 years) as well as San Francisco and Honolulu, two cities where residents need 40 years to save for a down payment. (The authors note that real estate in San Francisco is more expensive than Los Angeles but that wages in San Francisco are higher.)

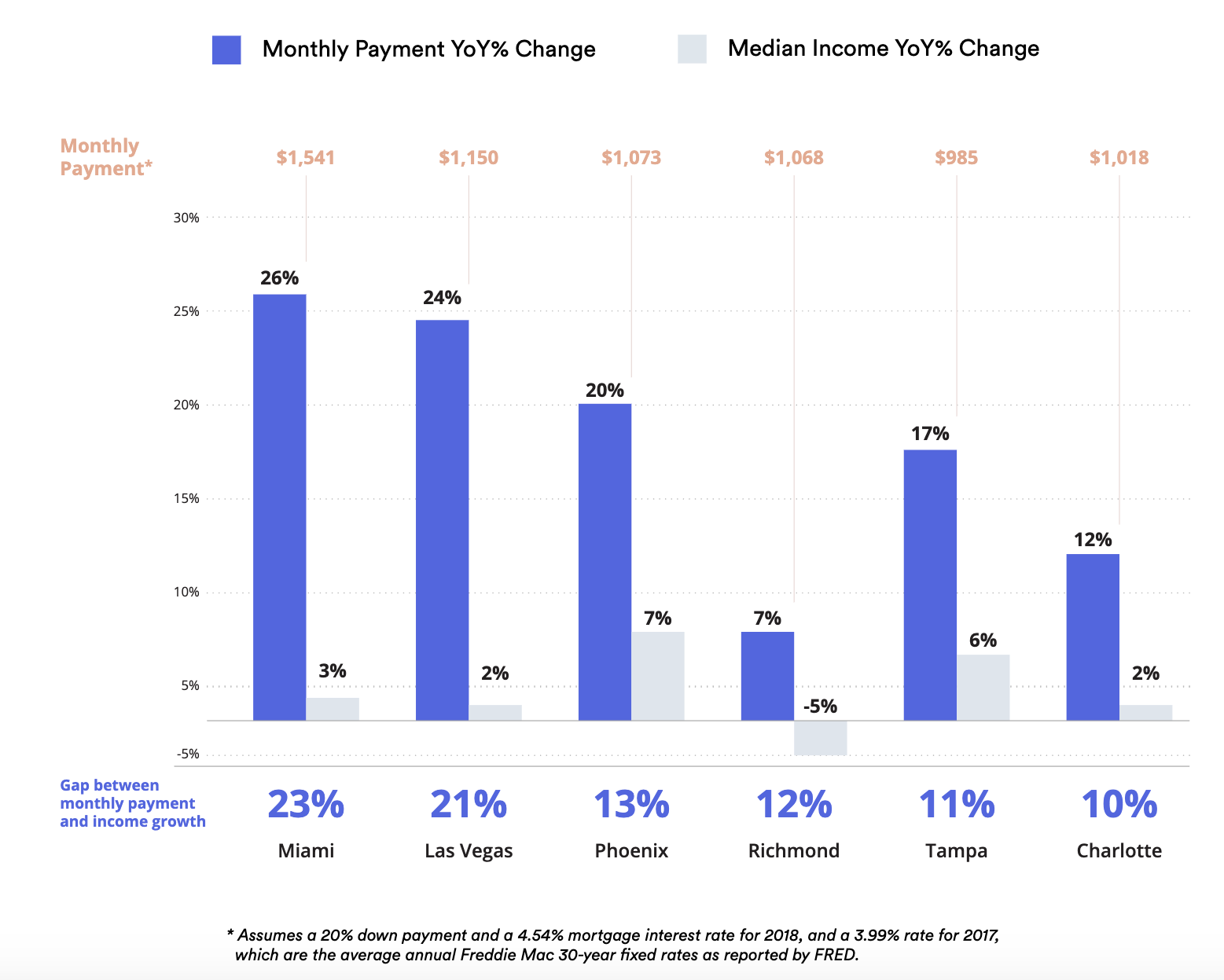

“The Miami and Las Vegas markets were particularly hot from 2017 to 2018, with median home values rising roughly three times the national increase of 6 percent,” the study says. “During the same time period, however, median incomes in Miami grew only 3 percent, hardly keeping pace with the housing market and making affordability further out of reach.”

According to Unison’s dataset, the typical mortgage costs $315,000 in the city of Miami, and a 20 percent down payment comes to $62,931.

The company notes that Miami also tops the nation in monthly mortgage-payment growth from 2017 to 2018 – and wage growth doesn’t even come close to keeping up:

Unison

There are a few caveats: The firm is relying on data only from the city of Miami and not all of Miami-Dade County, which has a higher median household income than the city. The city’s median household income is an insanely small $35,221 compared to the county’s also-paltry $49,930.

Of course, the Unison study is also a clear piece of advertising – the San Francisco-based firm, formerly known as Compusearch Software Systems, recently nauseatingly rebranded itself as being run by self-described “radical enablers of enlightened capitalism.” The company sells a service that supposedly helps people afford down payments, so it’s incentivized to make customers feel like homeownership is difficult. So take this study with a grain of salt.

But the company also isn’t lying that Miami’s real-estate market is essentially broken. The Miami Herald is midway through a series on the city’s affordability crisis, a topic New Times has also been harping on for years. State lawmakers have squandered affordable-housing funds and banned towns from raising their own minimum wage. Cities have refused to enact laws mandating affordable housing in distressed parts of town.

According to the recent Herald series, wages in Florida remain low even for skilled workers. But the Magic City’s housing prices remain remarkably high thanks to a market of foreign investors waiting to snatch up luxury homes near the beach. In essence, the city’s housing market is working – but not for the people who live here.