Wyn Van Devanter via Flickr Creative Commons

Audio By Carbonatix

Miami real-estate analyst Andrew Stearns releases a report about the health of the city’s condominium market four times per year. Read between the lines of Stearns’ last three consecutive releases, and it’s easy to picture him pulling out clumps of his hair and nervously loosening his tie as he writes the reports.

In the past year, Stearns’ predictions for the city’s “preconstruction” condo market have gone from bad to worse to, as of yesterday, apocalyptic. Stearns has warned for close to 12 months that Miami property brokers can’t sell all the new condos that developers are building. But in a new report issued yesterday, Stearns officially labels Miami’s units for sale that haven’t yet been built as “distressed.”

“The preconstruction condo resale market will likely continue to weaken as more units are delivered into the distressed market,” Stearns writes. “Building inventory and declining sales usually result in downside pricing pressure. Preconstruction condo developers, flippers, and existing condo resellers should expect pricing pressure to accelerate.”

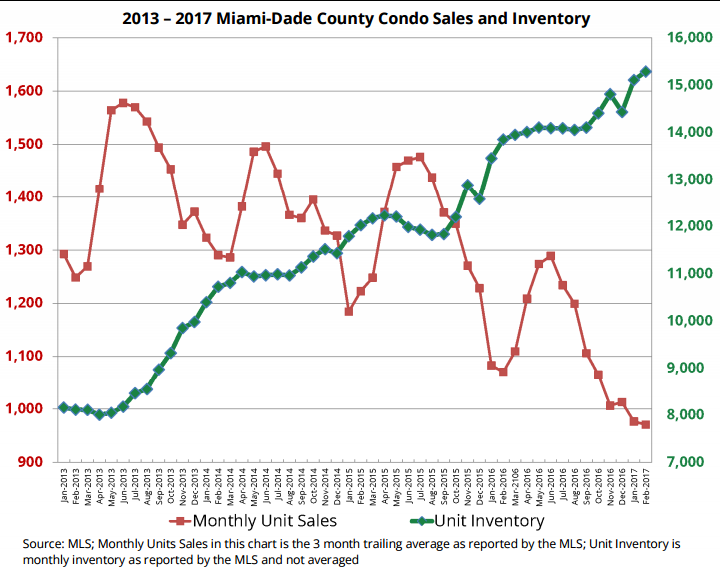

Stearns includes a gulp-inducing chart in his report, which shows condo sales have slumped like a black-diamond ski slope, right as inventory has hit an all-time high:

StatFunding

Stearns writes that from 2012 to 2015, new condo buildings typically sold out within months of completion. Now buildings are sitting on the market for months or years with empty units. The Crimson Miami in Edgewater, for example, is still 34 percent empty despite the fact that construction ended in December 2015. Rise at Brickell City Centre, part of a billion-dollar project that city officials hope will bring a “huge infusion of value” to the area’s tax coffers, is still 54 percent empty. Construction was completed there in September 2016.

Update: The ownership at

Brickell, which has been so rapidly infused with condo buildings postrecession that the towers now blot out the sun at ground level, seems to be getting hit the hardest in terms of unsold inventory. The neighborhood is a glittering monument to oversupply.

“Developers may resort to mark-down liquidations or bulk sales of unsold condo units as the cycle progresses, and time will tell how doing so will affect the

More than 11,000 new condo units are set to go up for sale by 2018. There is one potential silver lining to the crisis: If those condos are converted to apartment units, they could help bring down the city’s average rent costs. Given Miami’s concurring residential rent crisis, that would certainly be a positive.

But for Miami’s economy, Stearns’ new report is the latest warning sign. The report comes just as the Miami Herald reports that fear from Donald Trump’s travel ban and the Zika crisis have led to huge slumps in the city’s tourism economy. Hotel taxes have sunk every month since September – a pattern not seen since the Great Recession.

Speaking with the Herald, Mark Lunt, a real-estate consultant at Ernst & Young, placed some blame on Trump, among other factors.

International tourism and real-estate investment also tend to drop in Miami when the U.S. dollar is

Stearns’ report contrasts sharply with a sunny condo-market review conducted by the City of Miami’s Downtown Development Authority (DDA), which suggested in February that, after a small price dip, condo costs will continue to skyrocket, to the point that every downtown unit will cost no less than $750,000 by 2025.

But now, both the Herald’s reporting and Stearns’ predictions suggest the largest pillars of Miami’s economy – tourism and real estate – appear to be in deep trouble.